> For the complete documentation index, see [llms.txt](https://blog.tactyc.io/llms.txt). Markdown versions of documentation pages are available by appending `.md` to page URLs; this page is available as [Markdown](https://blog.tactyc.io/product-updates/solving-liquidation-preferences-in-tactyc.md).

# Solving Liquidation Preferences in Tactyc

It took us a long time to solve this given:

(a) the complex nature of liq prefs, and

(b) the lack of a complete cap table and security information needed to accurately calculate exit proceeds within Tactyc

#### But first, what are Liquidation Prefs?

While the full description of liquidation prefs deserves its own blog post, [this article](https://learn.angellist.com/articles/liquidation-preference) provides a helpful overview. Very simply, liquidation prefs enable preferred shareholders to receive proceeds ahead of common shareholders.

> *The payout order is important because when startups fail or get sold for less than their valuation, there may not be enough funds leftover for all investors to get their money back. Liquidation preferences work to ensure investors holding the liquidation preference are made “whole” before common shareholders can cash in on their shares.*

#### **What we were doing before today.**

Up until now, the calculation of exit proceeds in Tactyc was relatively straightforward i.e. it was a straight-pro rata calculation.

> **Exit Proceeds** = **Ownership (%) at Exit** x **Aggregate Exit Valuation**

This doesn’t work for *downside* cases. For e.g. let’s say you have a 2x non-participating liq pref on a $2mm investment and own 5% of the company. If the company sold for $50mm:

* Tactyc’s exit proceeds calculation was $50mm x 5% = $2.5mm

* Actual exit proceeds based on liq pref = $4mm

So Tactyc was undervaluing the exit proceeds in cases where a liq pref exists. Given the common nature of liq prefs, this could have an impact on the projected TVPI and DPI metrics for the overall fund.

#### Why it took us so long.

For one, liq prefs are complicated. They could be participating or non-participating. If they are participating, they could be further capped or uncapped.

But the reason it took us so long to support liq prefs in Tactyc was that we **do not know the full cap table of the company.** So we do not have visibility into which shareholders have liq prefs and their terms, we were not sure how to determine the impact of these liq prefs. After all there could be multiple liq prefs and we need to understand how they relate to each other.

We also do not know the *security type* of each investment for e.g. a user may have a Seed investment that has a liq pref, but their Series A follow-on in the same company may not have a liq pref.

#### **How we solved this.**

> *The “aha” moment was when we realized that despite not knowing the full cap table or security detail, we could still calculate the impact of liq prefs — if we only ask the user for **amount of liq prefs** on the cap table instead of the terms of each security and shareholder.*

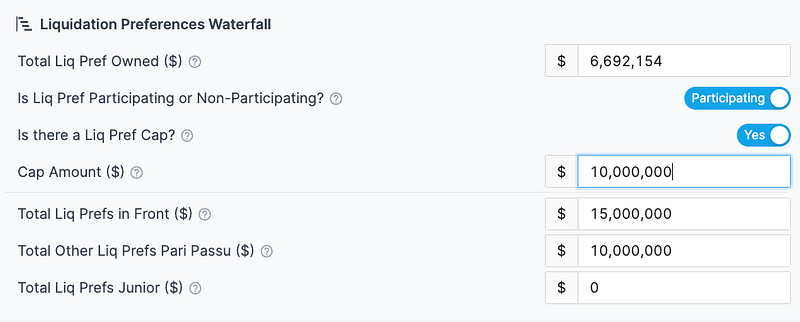

All we really needed to know was:

* **Amount** of liq pref owned by you and the type of liq pref owned by you (participating / non-participating / capped / uncapped)

* **Amount** of liq pref “in front” of you, “behind” you and pari passu to you.

By asking for amounts we can bypass the terms of the liq prefs. For example if an investor ahead of you has a 2x liq pref on their $5mm investment, the user can simply enter $20mm of liq pref “in front” of you.

We then calculate 3 cases for each exit:

* **Non-Participating Case with no Conversion:** We calculate a case where we assume you and your pari-passu investors don’t convert your liq pref. i.e. the amount available to you is the exit value reduced by the amount of liq prefs ahead of you.

* **Non-Participating Case with Conversion:** We reduce the exit value by liq pref senior and junior to yours — but assume yours (and your pari passu) investors convert their liq prefs.

* **Participating**: This is the easiest. We assume the exit value is reduced by everyone’s liq prefs — and you get to “double dip” by also participating in the common pool based on your pro-rata ownership %.

..and the final exit proceeds we show in Tactyc is based on the type of liq pref the user has specified.

#### Disclaimer

We acknowledge that there may be certain edge cases where investors may have other special rights or warrants that change the exit proceeds. However for the majority of our users, the above waterfall methodology should help them more accurately plan for exits with liq prefs.

By [Tactyc](https://medium.com/@tactyc) on [December 1, 2022](https://medium.com/p/123ec5f474c8).